Switching to a generic drug can cut your prescription costs by 80% or more - but only if you know what to ask. Many people think all generics are the same, but that’s not true. There’s a big difference between a traditional generic and an authorized generic, and how your insurance treats each one can mean the difference between paying $5 or $50 a month. If you’re spending too much on prescriptions, asking the right questions at the pharmacy could save you hundreds a year.

What Exactly Is a Generic Drug?

A generic drug is an FDA-approved version of a brand-name medication. It has the same active ingredient, strength, dosage form, and route of administration. The FDA requires generics to be bioequivalent, meaning they work the same way in your body as the brand-name drug. That’s not marketing speak - it’s science. A 2021 FDA analysis showed that within a year of a generic entering the market, prices typically drop by more than 75%. For some drugs, like the diabetes medication metformin, the price fell from $120 a month to under $5. But here’s the catch: just because a drug is generic doesn’t mean it’s cheap for you. Your out-of-pocket cost depends on your insurance plan’s formulary - the list of drugs it covers and at what cost tier. Some plans put generics in the lowest tier (often $5-$10), while others treat them like brand-name drugs if they’re not on the preferred list.What Is an Authorized Generic?

An authorized generic is different from a regular generic. It’s made by the same company that makes the brand-name drug, but sold under a generic label. Think of it like a car manufacturer selling the exact same vehicle under a different nameplate. The pills, packaging, and manufacturing process are identical. The only difference? The label says "generic" instead of the brand name. Why does this matter? Because authorized generics often have lower list prices than the original brand. A 2022 study in JAMA Internal Medicine found that authorized generics for drugs like Epclusa and Harvoni had list prices 50-67% lower than the brand. But here’s the twist: insurance companies and pharmacy benefit managers (PBMs) sometimes treat authorized generics differently than traditional generics. Some plans don’t apply the same discounts or rebates, which can mean your copay stays high even when the list price drops.Why You Should Ask About Authorized Generics

Most people never ask if their drug has an authorized generic version. But if you’re paying $45 for a brand-name drug and your pharmacist says, "There’s a generic for $30," you might still be missing out. The authorized version could be priced even lower - sometimes under $20. In 2022, the Association for Accessible Medicines reported that 93% of generic prescriptions had copays under $20. But only 59% of brand-name prescriptions did. That gap exists because generics are cheaper to produce. But if your insurance treats an authorized generic like a brand drug, you might pay the same as before. For example, a patient on insulin might switch from a $350 brand to a $90 authorized generic - but if their plan doesn’t recognize the AG as a preferred generic, their copay could still be $45. Meanwhile, another patient switching to a traditional generic might drop from $45 to $25 because their plan gives better coverage to non-AG generics.

How to Ask the Right Questions at the Pharmacy

You don’t need to be a pharmacist to get the best deal. Just ask these four questions every time you fill a prescription:- "Is there a generic version available?" - This is step one. If the answer is no, ask why. Some drugs, especially complex ones like inhalers or injectables, still lack generics.

- "Is this an authorized generic?" - If yes, ask if it’s listed differently on your insurance formulary than other generics.

- "How does my plan treat authorized generics versus traditional generics?" - This is the key question. Some plans put AGs on a higher tier because they’re made by the brand company.

- "Can I save money by switching between generic types?" - Sometimes, a traditional generic costs less than the authorized one, even if the list price is higher. It depends on your plan’s rebate structure.

Use Tools to Compare Prices

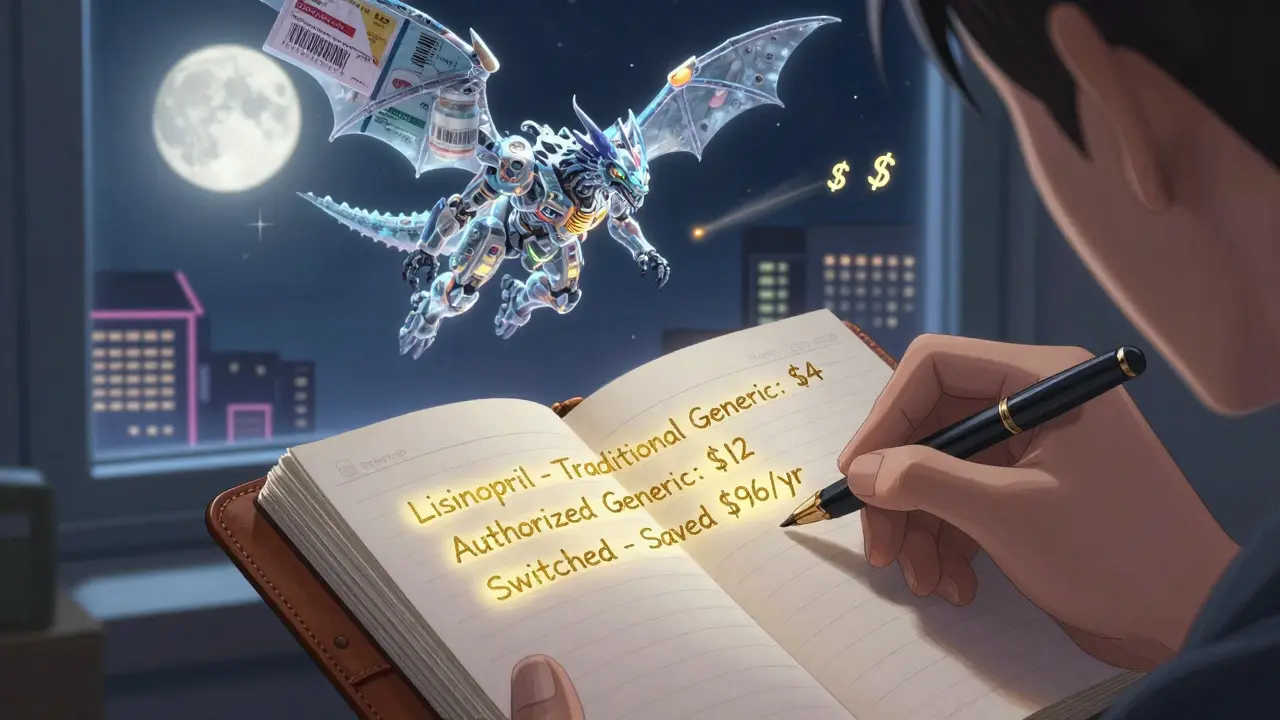

Don’t rely on your pharmacist’s word alone. Use free tools like GoodRx or SingleCare to compare cash prices for different versions of the same drug. You might find that the traditional generic is cheaper than the authorized one - even if the manufacturer says otherwise. For example, a patient on the blood pressure medication lisinopril found that the traditional generic cost $4 at CVS, while the authorized version was $12. Why? Because CVS’s contract with the PBM gave them a better rebate on the traditional version. The patient switched and saved $8 a month - $96 a year.

Why Some Generics Still Cost a Lot

Not all generics are created equal. Some drugs have very little competition - even after patents expire. The FDA reported in 2022 that 110 generic drugs had less than a 10% price drop after approval. Why? Because only one or two companies make them. When competition is low, prices stay high. This is especially true for complex drugs like inhalers, skin creams, and injectables. These are harder to copy, so fewer companies enter the market. The FDA’s 2023 Drug Competition Action Plan is trying to fix this by speeding up approvals for these tricky products. Also, high-deductible health plans can make generics feel expensive. Even if the drug costs $5, you might pay the full $5 until you hit your deductible. That’s not the fault of the generic - it’s the structure of your insurance.What You Can Do Today

Here’s your action plan:- Check every prescription you refill. Ask about generics and authorized generics.

- Use GoodRx to compare cash prices for all versions of your drug.

- Call your insurance plan’s pharmacy services line. Ask: "Is my drug on the preferred generic tier? What’s the difference between traditional and authorized generics under my plan?"

- If your copay is still high, ask your doctor if you can switch to a different drug in the same class - sometimes, another generic has better coverage.

- Keep a log: write down the name of the drug, the version (brand, AG, traditional generic), and your copay. Over time, patterns will emerge.

Real Savings Are Real

In 2022, generic drugs saved the U.S. healthcare system $408 billion. That’s $1,200 per person on average. But if you’re not asking the right questions, you’re not getting your share. The savings are there - they’re just hidden behind insurance formularies, rebate deals, and confusing labeling. The bottom line? Don’t assume. Don’t guess. Ask. Even if you think you’re already on the cheapest option, you might be missing a better one. It takes two minutes to ask. It could save you hundreds.Are authorized generics the same as brand-name drugs?

Yes, authorized generics are chemically identical to the brand-name drug. They’re made in the same factory, using the same ingredients and processes. The only difference is the label - it says "generic" instead of the brand name. The FDA requires them to meet the same strict standards as traditional generics.

Why is my authorized generic more expensive than the traditional generic?

It’s not the drug - it’s your insurance. Some pharmacy benefit managers (PBMs) treat authorized generics differently because they’re made by the brand company. Even though the list price is lower, your plan might not apply the same discounts or rebates it gives to traditional generics. This can result in higher copays. Always compare cash prices with GoodRx and ask your insurer how they classify each version.

Can I switch from a brand-name drug to a generic without my doctor’s approval?

Yes - but check with your doctor first. Pharmacists can substitute a generic for a brand-name drug unless the prescription says "dispense as written" or "do not substitute." However, for some medications - like seizure drugs or thyroid hormones - even small differences in absorption can matter. Always talk to your doctor before switching, even if the FDA says they’re equivalent.

Do generics work as well as brand-name drugs?

Yes. The FDA requires all generics to prove they’re bioequivalent - meaning they deliver the same amount of active ingredient into your bloodstream at the same rate as the brand. Studies show no meaningful difference in effectiveness or safety. A 2021 FDA review of over 1,000 generic drugs found no evidence that they underperform brand-name drugs.

Why don’t pharmacies tell me about authorized generics?

Many pharmacists aren’t trained to explain the difference between authorized and traditional generics. Their job is to fill the prescription, not to navigate complex PBM rebate structures. A 2022 survey found only 43% of independent pharmacists could clearly explain how authorized generics affect pricing. That’s why you need to ask - don’t wait for them to bring it up.

Kancharla Pavan

February 17, 2026 AT 01:14Let me get this straight - you're telling me we're all being scammed by Big Pharma and their puppet PBMs while pharmacists sit there like dumb statues? This isn't just about generics, this is systemic exploitation. The FDA's 'bioequivalence' standards are a joke. I've seen patients on insulin switch to generics and have seizures because the inactive ingredients changed. They don't test for bioequivalence in real human bodies, only in test tubes. And don't even get me started on how the same factory produces both brand and 'authorized generic' - that's not transparency, that's corporate fraud dressed up as savings. You think GoodRx helps? It's just another middleman taking a cut while the real savings go to shareholders. This whole system is rigged and you're just telling people to ask nicer questions. Pathetic.

Digital Raju Yadav

February 17, 2026 AT 10:50India produces 20% of the world's generics and we're still being told to beg for scraps? This whole 'authorized generic' nonsense is a US-only scam. In India, we don't care if it's branded or generic - if it's FDA-approved, we take it. Your insurance system is broken because you let corporations write the rules. We have medicines here that cost 1/10th of what you pay and they work better. Why? Because we don't have 17 different middlemen siphoning off profits. Your 'savings' are imaginary because your system is designed to keep you poor. Stop asking nicely. Start demanding accountability. Or move to a country where medicine isn't a luxury.

Carrie Schluckbier

February 19, 2026 AT 09:06They're lying to you. All of it. The FDA? Controlled by Big Pharma. GoodRx? Owned by private equity firms that profit when you pay more. That 'authorized generic' you think is cheaper? It's probably made in the same plant as the brand, but the PBM forces the pharmacy to charge you more because they get kickbacks from the brand company. I've seen the documents. There's a whole network of shell companies routing rebates so you never see the savings. And they call it 'transparency'? They're laughing at you while you're saving $5 on a $45 pill. Your doctor doesn't know. Your pharmacist doesn't know. Even the people writing these articles don't know the real game. You're being played. Always.

guy greenfeld

February 19, 2026 AT 16:33There's a deeper existential crisis here, isn't there? We've reduced human health to a transactional algorithm governed by rebate structures and formulary tiers. The very notion of 'saving money' on medicine implies that health is a commodity rather than a right. The authorized generic isn't just a pharmaceutical variant - it's a metaphor for our society's abandonment of care in favor of cost-efficiency. We've replaced compassion with spreadsheets. We've replaced trust with fine print. And now we're told to 'ask nicely' to get back what was stolen from us. The real question isn't how to save $5 on a prescription - it's why we've allowed a system where a person's life depends on whether their insurance company has a better deal with manufacturer X than manufacturer Y. This isn't healthcare. This is capitalism with a stethoscope.

Adam Short

February 21, 2026 AT 11:48My God, this is why Britain left the EU. Not over borders or trade - over medicine. You think we didn't have this problem? We did. Then we said NO MORE. The NHS doesn't care about 'authorized generics' or 'PBMs' - it just buys what works and charges £1.90. You Americans are so obsessed with your 'system' that you've forgotten how to just... fix things. This whole thread reads like a financial analyst's fever dream. You're overcomplicating a simple solution: make medicine affordable. Not negotiate. Not ask. Just make it cheap. We did. You're still stuck in your spreadsheet hell. Sad.

Agnes Miller

February 22, 2026 AT 00:44Just wanted to say I tried this and it WORKED. My dad was paying $42 for his blood pressure med. Asked about authorized generic - turns out it was $11 cash at Walmart. Switched and saved $360 a year. No magic, no conspiracy - just asking. Also, I always use GoodRx AND check the pharmacy's internal discount program (some have them!). And yeah, sometimes the traditional generic is cheaper. I keep a little notebook. Took me 3 tries to get it right. Don't overthink it. Just ask. It's not hard.

Geoff Forbes

February 23, 2026 AT 06:03Let me break this down for you with bullet points since you clearly can't handle nuance: 1. Authorized generics are not 'cheaper' by default. 2. Insurance formularies are not 'rigged' - they're complex. 3. GoodRx doesn't 'lie' - it's a price comparison tool. 4. Pharmacists aren't 'incompetent' - they're overworked. 5. Your 'savings' are conditional on your plan's contract with your PBM. Stop treating this like a moral crusade and start treating it like a financial optimization problem. You're not a victim. You're a consumer. Act like one.

Jonathan Ruth

February 24, 2026 AT 07:37Yall are overthinking this. Ask the pharmacy if there's a generic. If yes ask if its authorized. If yes ask how your plan treats it. If it's still high check GoodRx. If GoodRx is cheaper buy cash. Done. No drama. No conspiracy. No philosophy. Just three questions and one app. You're not fighting Big Pharma. You're just buying medicine. Stop making it a movement.

Philip Blankenship

February 25, 2026 AT 13:58Man I love how this thread went from 'how to save money' to 'the capitalist system is evil' to 'just ask your pharmacist'. Honestly? The truth is somewhere in the middle. I used to be the guy who just took whatever the pharmacy gave me. Then my wife got diagnosed with hypothyroidism and we started digging. Turns out there's like 5 different versions of levothyroxine out there and they're not all the same even if the FDA says they are. We found out our plan covered one generic better than the other. We switched. Saved $180 a year. Now we ask every time. It's not a revolution. It's just being smart. And yeah, pharmacists don't always know. They're busy. So you gotta be the one to ask. No shame in that. Just do it. You'll thank yourself later.